2020 to 2030 will see the Industrial Internet thrive. Leading global carriers must innovate new intelligent, digital services, transform their business models in the new arena and achieve new growth in vertical industries.

By Li Changwei, Huawei Carrier BG

Internet companies have thrived during the decade of the mobile Internet. Microsoft, Apple, Google, and Amazon had a combined value of US$6 trillion in 2021, and Apple was valued at US$3 trillion in 2022. In contrast, the telecom industry experienced a period of decline, with its growth rate dropping to 2%–3%. GSMA predicts that if carriers continue the "dumb pipe" business model, the growth rate will be only 1.5% between 2021 and 2027, and that the market space will not exceed US$2 trillion in 2027, despite a booming Industrial Internet.

What should the telecom industry do? The answer is transformation.

The Industrial Internet: A blue ocean with challenges

New technologies like 5G, cloud, big data, artificial intelligence, and IoT are creating a new wave of Industrial Internet innovation and development. Driven by national digital economy strategies, the Industrial Internet will become the biggest blue ocean for new growth.

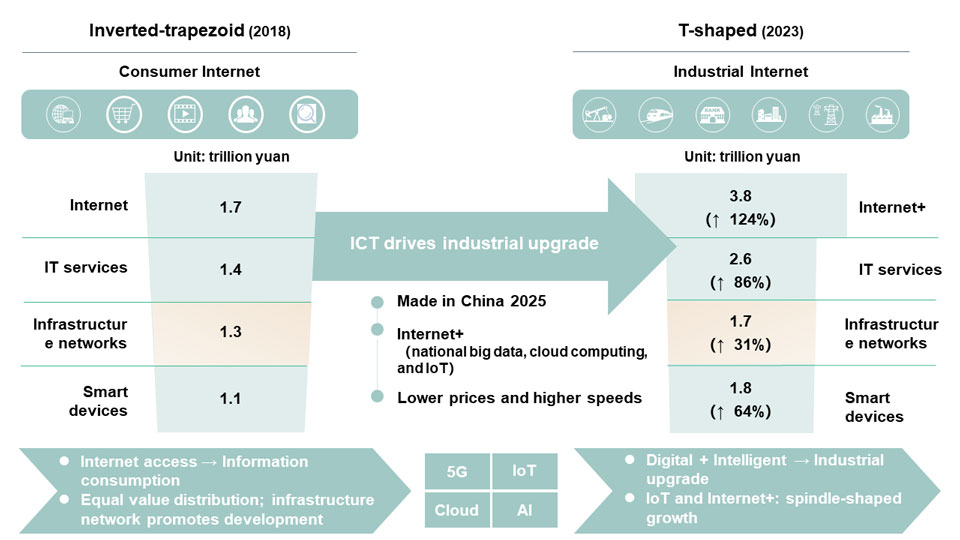

Figure 1: Industrial Internet market space analysis

In the Industrial Internet era, carriers must draw from their experience and lessons learned in the mobile Internet era. They should build optimal gigabit networks and high-quality connections, actively extend their service capabilities to vertical industry ecosystems, and develop industry solutions through open cooperation and innovation. This is the only way they can create new business models and new value in new domains. During the past decade, leaders of the information industry have entered the strategically important B2B industry. Global carriers such as AT&T, Telefonica, and Vodafone; Chinese carriers, including China Mobile, China Telecom, and China Unicom; and Internet companies like Amazon and Alibaba have chosen between the strategies of integration or being integrated. They have also forged partnerships. Some of these attempts have succeeded, some have failed.

In October 2016, Alibaba’s Jack Ma proposed the five “new” strategies of new retail, new finance, new manufacturing, new technology, and new energy. He hoped to make use of middle platforms to quickly integrate and break through industry markets. But, in fact, these new domains have been fed by Alibaba's core e-commerce business. This reveals the challenges facing B2B innovation. Huawei has also adjusted its B2B market strategy from integration and being integrated to establishing integrated teams. Currently, Huawei is still exploring its B2B strategy as it moves forward.

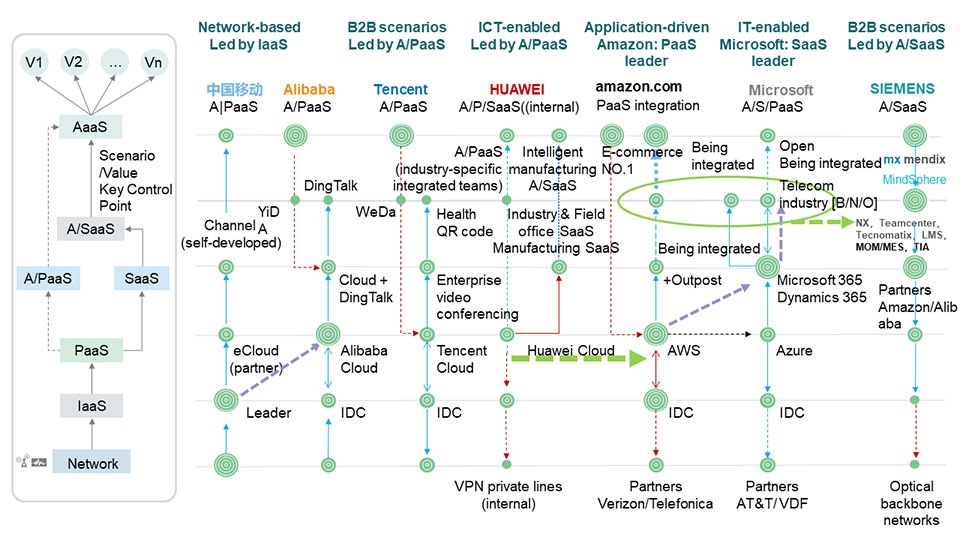

Figure 2: A/SaaS solution innovation strategy in the B2B domain

Carriers lack the ability to develop integrated solutions for core B2B markets and have not established differentiators in services. A lack of strategic control points leads to unclear profit models, making it difficult for B2B business to support sustainable development and growth.

What is a way out for carriers in the B2B market?

Four B2B market transformation and breakthrough strategies

We have proposed four B2B market transformation and breakthrough strategies by considering B2B business from a global and industry perspective. These strategies assess carriers' success in terms of business scale and profits.

Model 1: PaaS integration

E-commerce has driven the cloud innovation and iteration of AWS, allowing Amazon to lead the world in PaaS performance, efficiency, cost, security, and openness. Governments, banks, and top OTT players have all selected AWS for cloudification and digitalization. With strong capabilities in application as a service (AaaS) and SaaS, top enterprises, government agencies, and OTT players in the US have led the integration of Amazon's PaaS system. This helped streamline the industry value chain and enabled the iteration and operations of applications and services. The secret to Amazon's high profitability from PaaS lies in the aggregation and contribution of top customers, which creates a virtuous cycle for its B2B business.

Model 2: SaaS integration

While trailing Amazon in the PaaS space, Microsoft identified market demand and opportunities for SaaS, integrating Azure into its own software systems such as Windows, Dynamics 365, Office 365, and LinkedIn. This helped Microsoft become a leader in enterprise SaaS solutions and rapidly expand its enterprise market. For the industry market, Microsoft built the Power Platform based on SaaS, on which industry customers can develop applications from the top down, create new B2B solutions by integrating enterprise SaaS, and make breakthroughs in AaaS.

Model 3: Innovative A/PaaS model

Alibaba's Zhejiang e-government DingTalk team and Huawei's integrated teams leveraged their strong PaaS capabilities to enter the B2B market. They developed innovative scenario-based applications, including video surveillance, drones, and AR applications, that relied on cloud, big data, and AI PaaS platforms, creating new business models. The A/PaaS model simply connects the SaaS systems of industries rather than overhauling these systems. Due to limited value to the scenarios it supports, this model is only an innovative choice for markets that lack software autonomy, as it does not deal with core software. The A/PaaS model can be used only in limited scenarios and lacks core competitiveness.

Model 4: Innovative A/SaaS solution from inside out and top down

Siemens' intelligent manufacturing solution is an innovation driven by IoT application scenarios in the manufacturing industry. Siemens has a powerful industrial software SaaS platform and capabilities. To integrate data technologies and new IoT technologies and transition into digital and intelligent manufacturing, Siemens developed Mindsphere, an IoT application innovation platform. With Mindsphere, different IoT devices, including intelligent control robots, robotic arms, AGVs, and sensors, can be developed to build AaaS platform capabilities. Siemens also used Mindsphere to develop Mendix, a low-code IoT application development platform that helps partners develop customized applications based on factory scenarios and foster an application environment. Siemens' digital and intelligent transformation strategy is to identify and focus on high-value IoT application scenarios. Based on technology maturity assessments, Siemens focused on innovative vertical solutions, developed new commercially replicable business models, and extended applications to other industries horizontally. The scenario-driven, value-oriented strategy helped Siemens surpass GE to become a role model of digital and intelligent transformation in the Industrial Internet era.

Huawei implemented a similar digital and intelligent transformation based on its advanced manufacturing system.

These success stories suggest that the key to B2B market transformations and breakthroughs is connecting vertical ecosystems, developing new services and applications that deliver value, and building A/SaaS solutions through open iteration and innovation with ecosystem partners.

Upgrading innovation from products to solutions

Major global carriers have been working in the B2B business for more than 10 years. Carriers in China, the US, and Europe mainly provide new products and technologies, such as networks, cloud, big data, IoT, artificial intelligence, enterprise private lines, and videoconferencing, as part of their integrated solutions. This model has helped carriers achieve rapid market growth in the early stages of technology deployment. However, as this model becomes more fragmented, the industry will face challenges to turn a profit. Carriers must upgrade B2B solutions, break through the critical point of B2B market value, and go beyond connectivity to achieve profitable business at scale.

To upgrade the B2B solution strategy, carriers need to build on their IaaS strengths in networks, cloud, data, security, and localized resources, and identify strategic businesses in the B2B market. They should also predict market demand and the maturity of opportunities; seek ecosystem partners, including leaders at the AaaS, SaaS, and PaaS layers; and choose an effective cooperation model between integration and being integrated so as to connect the vertical ecosystems of I-P-S-A solutions.

If carriers are integrators, they cannot provide competitive solutions due to a lack of expertise and control over vertical industries. If carriers want to have their solutions integrated as part of their overall offerings, then no one will be integrators due to a lack of leading application and software players in China's ICT industry.

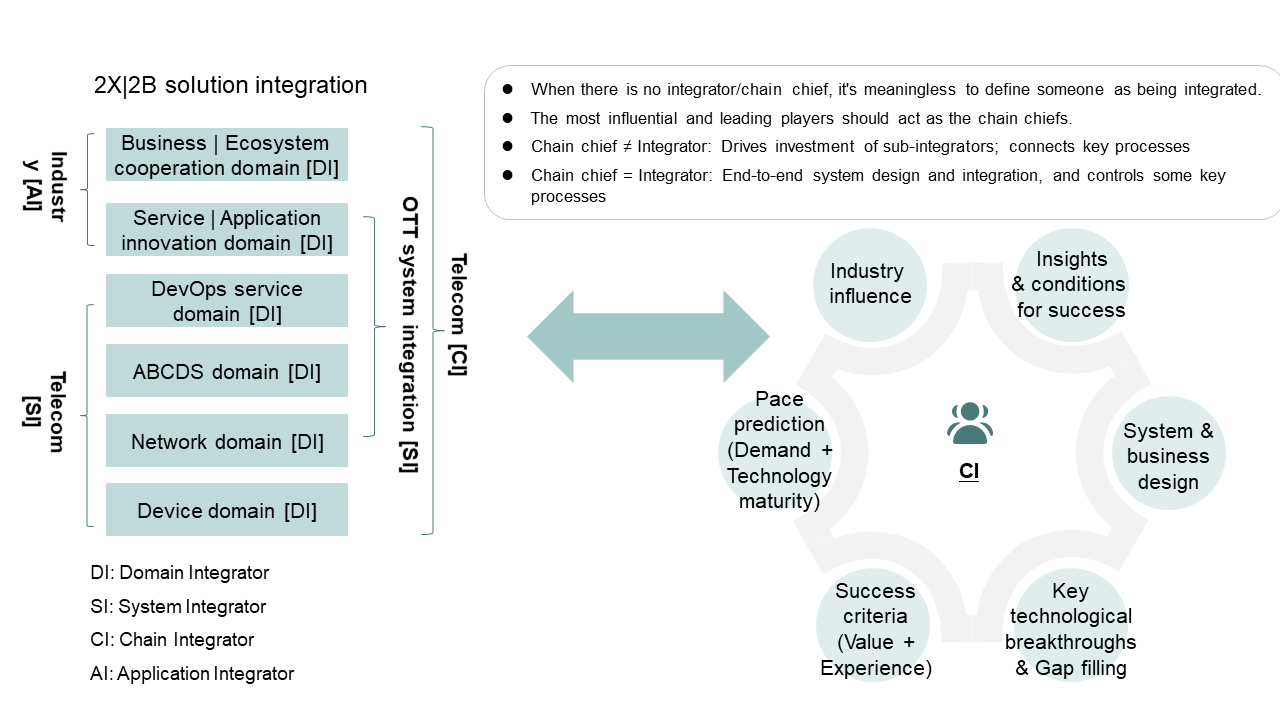

Figure 3: The "value chain chief" model enables B2B solution integration, innovation, and breakthroughs

As industry development hit new bottlenecks, the telecom industry recommended that carriers or industry leaders serve as "value chain chiefs", as the industry lacks integrators with leadership and end-to-end technical capabilities. This model will help form industry alliances to explore integration standards for solution architectures, applications, and modules. Following these standards, industry players can innovate and develop solutions on their own, with their solutions integrated to adapt to different scenarios under the leadership of the chief. This is like how different compartments of a bullet train work, as shown in Figure 3.

After breakthroughs are made, the chief can replicate end-to-end solution integration capabilities and transform into a solution integrator in the B2B industry, so as to achieve large-scale business expansion and create larger space for growth.

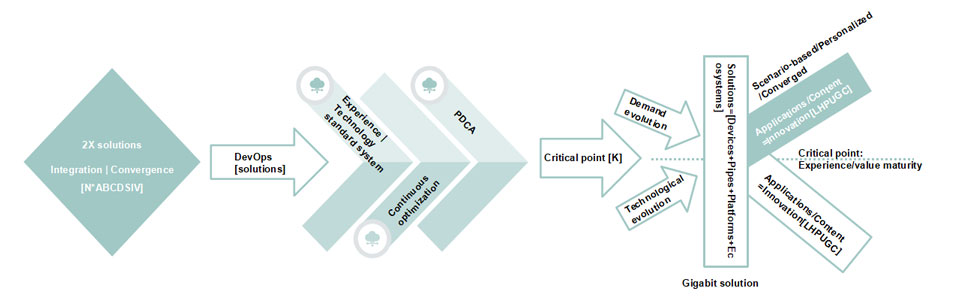

B2B solution innovation is a process of trial and error in different scenarios. The success of solutions should be measured by the critical point of value. The industry follows the "K-shaped" rule of value, as shown in Figure 4. The rule states that if the value of new business forms exceeds the critical point in the K-shaped model, they will have higher returns and more growth opportunities. If not, they will be rejected by the market. Carriers must select the right strategic direction and industries, and continuously iterate, optimize, and upgrade solutions to approach and even exceed the critical point of value. Carriers must possess innovation capabilities and a strong will to win.

Figure 4: Scenario-based B2B solution iteration and breakthrough of the critical point of value

Back to being value-oriented

The B2B market is essential for the telecom industry. To achieve success, the industry must generate more value for customers through innovation to optimize and upgrade previous businesses and replace them at scale.

While continuously pushing the limits of underlying technologies, carriers should carry out scenario-based, value-driven innovation, and identify key industry customers and new business requirements. They should serve as "value chain chiefs" or integrators to bring together the strongest partners along vertical ecosystems, and focus on high-value applications to develop innovative solutions that integrate devices, pipes, clouds, intelligent technologies, and security. This solution-based innovation model goes beyond the current platform-based innovation model by focusing on new applications, solutions, and platforms.

Carriers must refocus on market and customer needs, and identify strategic opportunities and the maturity of industries in different scenarios. Building on their strengths, carriers should establish cooperation models that adapt to industry development status in the vertical domain, and voluntarily act as the "value chain chief" to achieve business expansion at scale and bigger growth.