ChatGPT rocked the world in 2023, and now is the time to take a hard look at the current trends dominating AI development, innovation, evolution, and competition. Clearer insights into feasible directions and asymmetric competition strategies will be critical for China's AI industry as AGI draws near.

By Li Changwei, Chief Strategic Marketing Expert, Huawei

ChatGPT 3.0's launch in December 2022 was like the big bang for AI. Since then, development has continued at breakneck speeds, with new foundation models, including GPT-3.5 and GPT-4, shortly following and artificial general intelligence (AGI) just over the horizon. AI models now have more parameters than human brains have neurons, enabling models to make inferences in similar ways as humans do.

AI has become the key to competitiveness and leadership for the ICT industry in the intelligent era.

Breaking bottlenecks: AGI is approaching a critical point

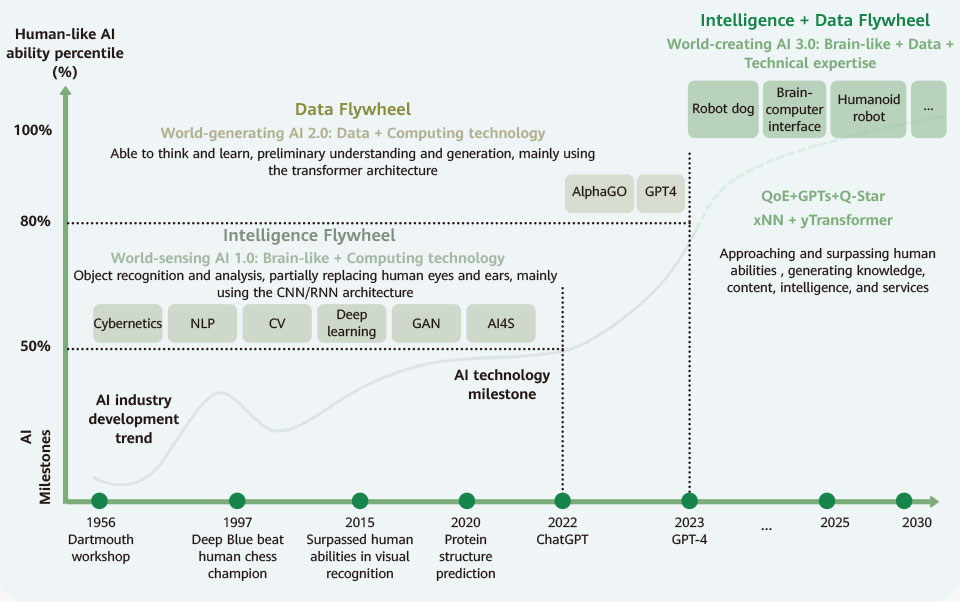

ChatGPT is propelling AI development forward using a model called the "data flywheel," which uses statistical algorithms rooted in calculus and probability theory. This leaves ChatGPT to deal with two challenges: accuracy and training costs. ChatGPT 3.5 was trained on 1.8 trillion parameters, costing nearly US$5 million per training cycle, but its accuracy bottlenecked at the 90th percentile (Figure 1).

Figure 1: The data + intelligence flywheel approach is driving the evolution from AIGC to AGI

To break through this bottleneck, OpenAI has adopted a new three-step strategy: First, adding specialized AI, or a Mixture of Experts (MoE), which means linking 16 specialized AI models with 110 billion parameters to the general AI foundation model which will improve its accuracy. Second, providing open ChatGPT APIs to encourage ecosystem partners to generate their own specialized GPTs based on GPT and develop specialized intelligent agents. Third, developing, integrating, and absorbing new algorithms, such as Q-Star, to get ever closer to AGI.

Tempted by the enormous market potential and the low market threshold, many major tech companies are increasing investment in AI. In 2023, Google introduced its multimodal model Gemini, which will help it move from AIGC to AGI. The Google DeepMind team also recently launched their FunSearch algorithm, which works by pairing a pre-trained large language model (LLM) designed to output creative solutions in the form of computer code with an automated "evaluator" that guards against hallucinations and incorrect ideas. By iterating back-and-forth between these two components, initial solutions "evolve" into new knowledge, gradually approaching what's required for AGI.

Once achieved, AGI will set the stage for AI to be truly integrated into enterprise operations. Microsoft's Copilot, for example, was launched as part of its Office apps, with ChatGPT pre-integrated. Enterprise users have flocked to this new service, despite its US$30 per month subscription fee, making it a new growth engine for Microsoft. Other current industry applications include Tesla's humanoid robot Optimus and autonomous driving system FSD V12, as well as Huawei's Pangu Weather foundation model, which have made breakthroughs in critical indicators, like industrial experience and accuracy, to shape new business models that boost efficiency across industries.

The turning point for AGI is almost here, according to many. NVIDIA CEO Jensen Huang anticipates the advent of AGI within the next five years, while Tesla CEO Elon Musk believes that AGI will come within three years.

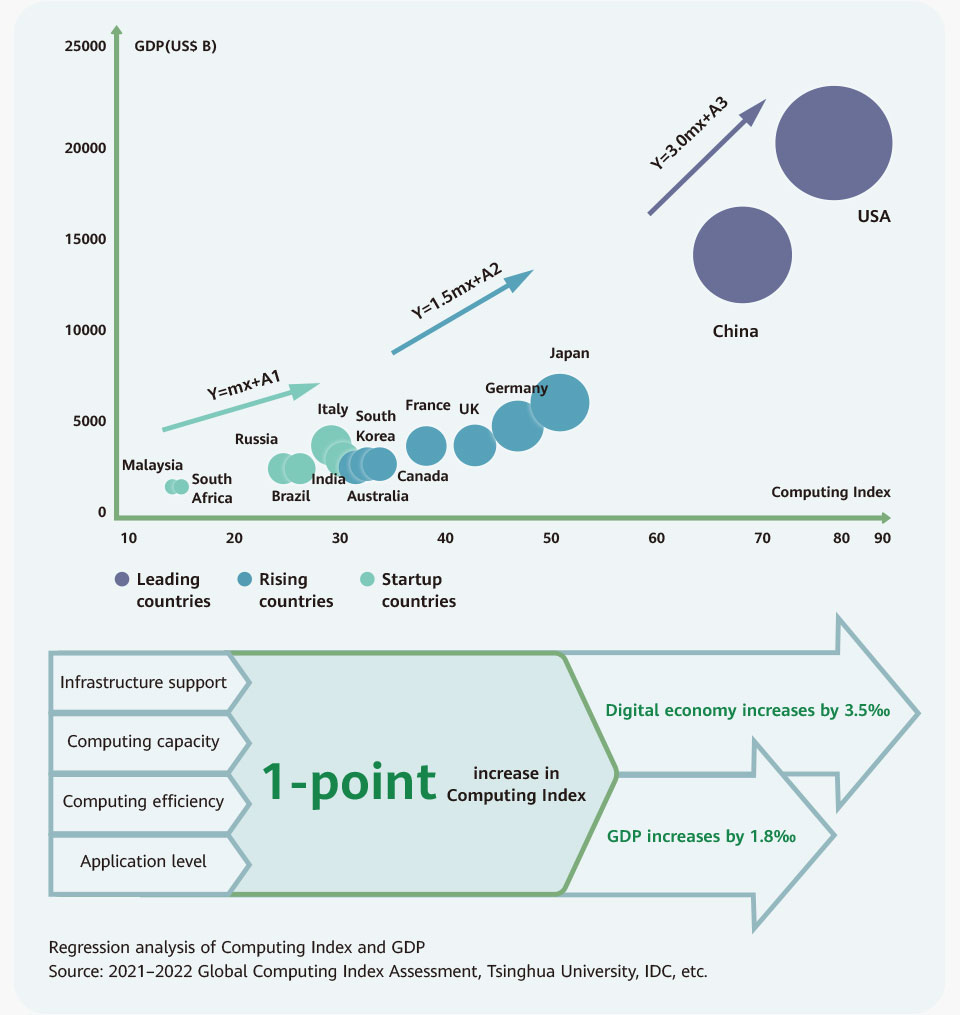

AI is already changing the paradigm of economic growth. According to China's Ministry of Industry and Information Technology, growth in AI computing scale can effectively drive growth in the digital and intelligent economy. They found that every 1-point increase in the Computing Index in 15 key countries correlated to a 3.5‰ and 1.8‰ increase in national economic growth and GDP, respectively. This new AI-driven economic development model will begin to impact global strategic competition in 2024. (Figure 2)

Figure 2: AI computing power is closely related to GDP

Differentiated leadership: The emerging path forward for AI

AI used to be seen as an open-source and non-profit technology. However, as it matures, it is increasingly found at the center of closed and business-oriented competition. Tech giants that used to collaborate with each other have become divided and focused on competition.

Major tech companies now either want to work with OpenAI, the biggest name currently in the game, or follow in its footsteps. Microsoft works extensively with OpenAI, outperforming everyone else in LLMs. Copilot was jointly launched by the two companies.

Anthropic, which has a different approach to AI safety, is now one of the biggest competitors of OpenAI. Google, whose search business faces the greatest risk of being replaced, has launched its own AI services including Bard and Gemini. Google has also taken advantage of YouTube's service data and algorithms to solidify its leadership in multimodal technology. The FunSearch algorithm recently launched by the Google DeepMind team now allows Google to potentially outperform other players in AGI. Tesla launched AI systems that are closely linked with its electric vehicles, such as FSD V12 and Optimus, to establish differentiated leadership. Meta AI has integrated more than 20 new AIGC methods, focusing on improving user experience related to search, social discovery, advertising, and business communication across its platforms, including Facebook, Instagram, Messenger, and WhatsApp. Apple is using AI to improve Siri and is expected to launch generative AI functions for its iPhones and iPads in 2024 with the release of iOS 18 and iPadOS 18. Finally, Amazon has leveraged its advantages in cloud to launch Titan AI, which includes text models for content generation and embedding models that can create vector embeddings for efficient search functions. Amazon also launched the CodeWhisperer, an AI coding assistant that is free to users.

Each of these tech giants has chosen a different way to develop AI. But together, they represent the convergence of AI, security, cloud, services, and devices, as all focus on innovation in scenario-based application experiences and value integration, which ultimately enables differentiated leadership.

Core AI players have added algorithms, like specialized AI, new Q-Star, and FunSearch, to data statistical analysis methods to maximize their strengths and move from driving exponential growth in AI computing demand to driving logarithmic growth.

China's approach: Strategy- and business-driven AI development

International tech giants are not the only ones pursuing AI development. China is doubling down in this field. The country's AI strategy is seen as critical to future breakthroughs in both the ICT industry and growth of the nation's digital economy. Generally, China's AI development has focused on strategy and business.

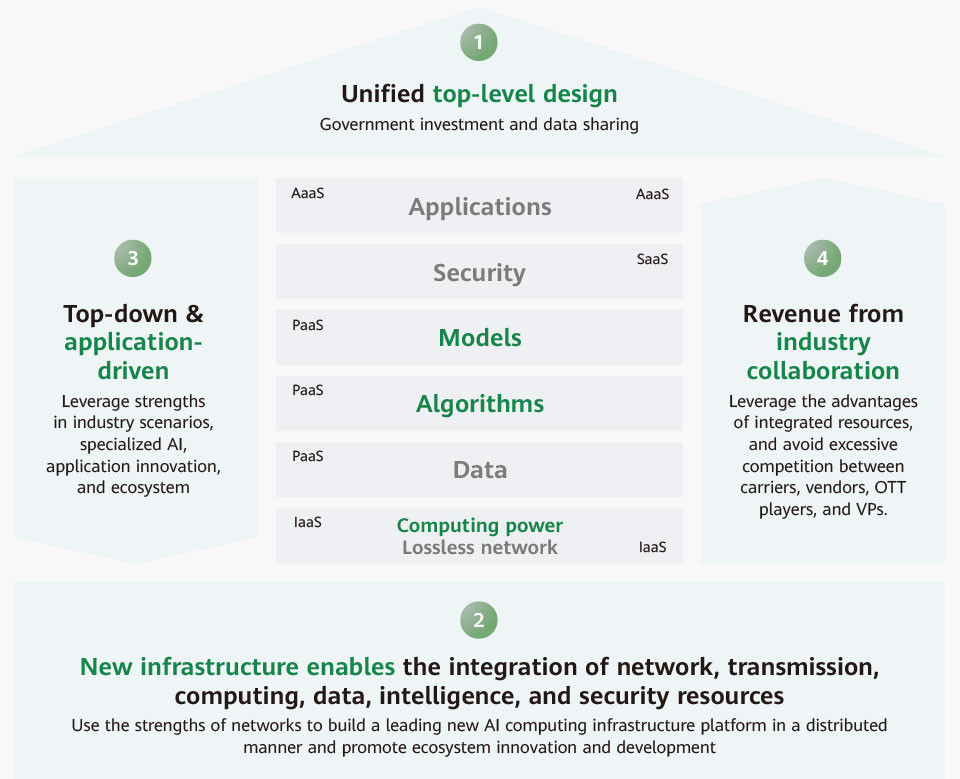

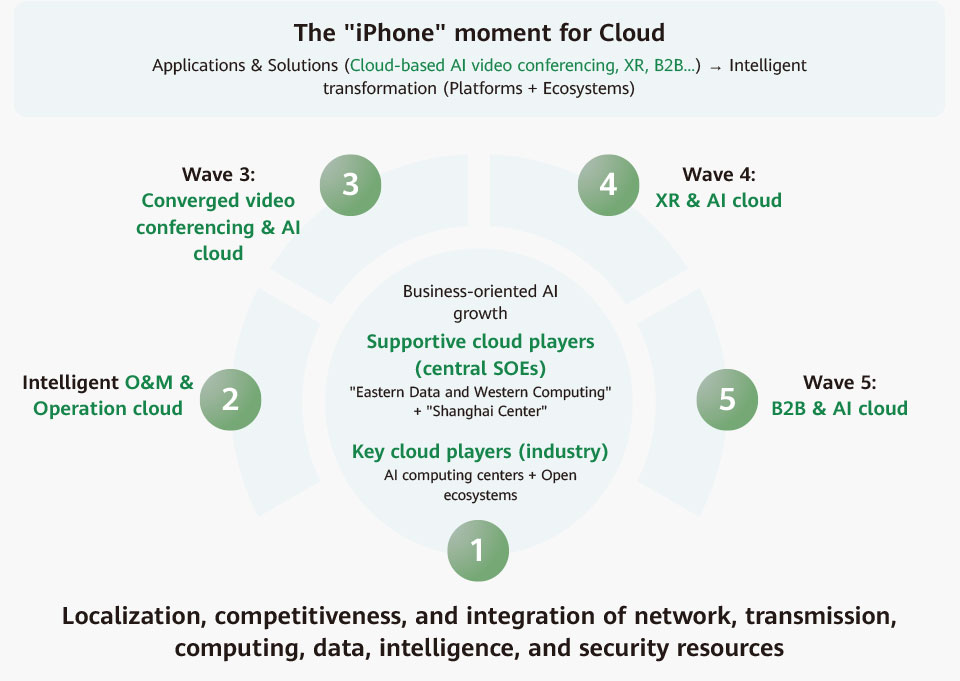

In terms of top-level strategy design, national resources and those of individual enterprises are being organized along specified development paths from the top down to achieve collaboration and boost industry revenue (Figure 3).

Figure 3: Government-led top-level design + Carrier-led new infrastructure + Application-driven + Industry collaboration

Early on, the government played a leading role through preferential policies, strategic investment, and data sharing. It started by setting digital security rules and application requirements for the government's own digitalization and intelligent application scenarios. Then, it turned to state-owned enterprises to promote the construction of new AI infrastructure by integrating network, transmission, computing, intelligence, and security elements. This is helping the nation to build an AI computing platform that will serve as critical infrastructure and promote both corporate and academic AI research and development. The aim here is to build a natural momentum that will drive development.

The government has also prioritized ecosystem integration and policy collaboration at the industry and enterprise levels to prevent excessive competition in AI foundation models at the PaaS layer and preserve breakthrough opportunities at the SaaS and application layers.

This top-level design is supposed to ensure an application-driven, top-down AI development path. Commercial breakthroughs are expected to be made thanks to China's diversity in low-level application scenarios and AI expertise in some domains. This will further encourage the development and quick adoption of smaller models, specialized AI applications, and innovative solutions (Figure 4).

Figure 4: AI foundation model services + New service planning

However, AI infrastructure is prioritized over applications in China so as to leverage the country's network advantages at the IaaS layer. AI computing clusters can make up for insufficient single-point computing power and integrate scattered computing resources to power the upgrade and iteration of developing and verifying AI foundation models. Carriers are prime representatives for state-owned enterprises (SOEs) here, and are expected to replicate NVIDIA's AI Foundations strategy while building new AI computing centers. They will be able to turn a profit by enabling technology companies and scientific research institutions and by leasing AI computing resources.

By expanding and strengthening AI computing centers, they will be able to implement "inside-out" service enablement, where carriers upgrade their primary commercial services through AI-based service integration, while achieving real growth in new market segments.

Microsoft has simplified complex service management capabilities through AI-based integrated operations, which can be a big help here. For example, network automation can help carriers simplify network management and improve customer services. SKT in South Korea has set a benchmark for this kind of strategic AI transformation. In November 2022, SKT CEO Ryu Young-sang announced the company's plan to become an AI company. It has since worked with partners to develop a Korean large language model, which is similar to GPT-3. In May 2022, SKT also launched a Korean AI chatbot "A.", attracting more than 1 million users. At MWC 2023, SKT showcased numerous intelligent services based on foundation models. These services include companion AI, data AI, visual AI, medical AI, and urban air mobility (UAM). SKT's key advantages over other carriers here is that it possesses both telecom know-how and proprietary local data that OpenAI does not have.

New MaaS: The AI collaboration strategy for carriers

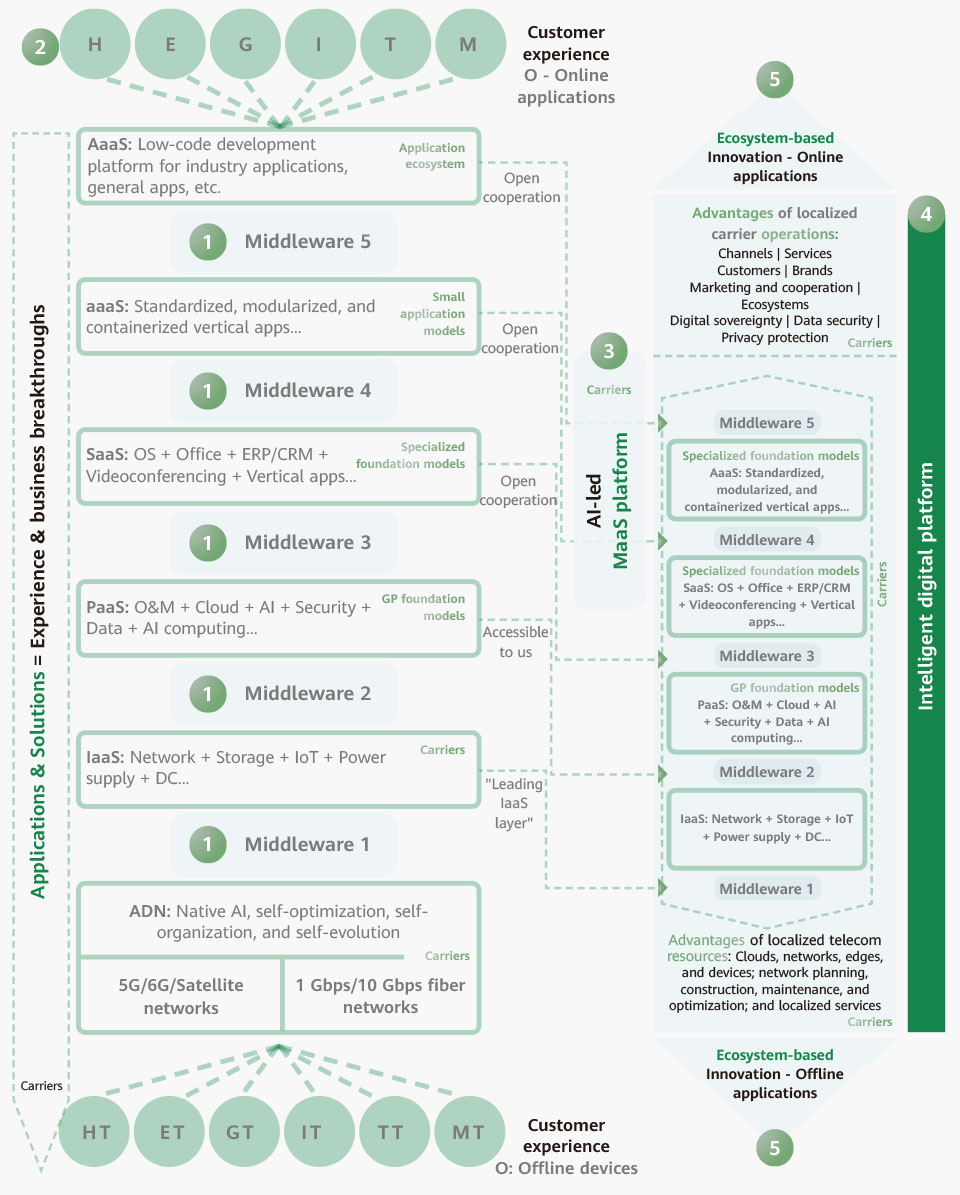

For carriers, intelligent digital platforms play a key role in integrating telecom services with AI. This is how they create new capabilities and competitiveness in networks, operations, and O&M. As the foundation of intelligent digital transformation for carriers, cloud and intelligent technologies make networks, computing power, and service configurations more flexible, efficient, and affordable. This has increased their focus on a large number of multi-service scenarios (Figure 5).

Figure 5: Transforming MaaS to build an intelligent digital platform and ecosystem leadership

When it comes to AI collaboration, carriers are now focusing their strategies on integrating their vertical industry value chain resources (security, data, and networks) to form a new Model as a Service (MaaS). Under it, layer-1 XaaS technologies and capabilities are provided and supported by leading technology vendors. Carriers, on the other hand, focus on the second layer where they develop middleware to integrate XaaS at each layer. This new MaaS encapsulates and integrates vertical elements throughout the value chain leveraging operation and infrastructure advantages.

MaaS will serve as the broad infrastructure that underpins the AI era, providing secure, efficient, and low-cost model usage and development support for downstream applications. Carriers will direct this usage, as they will provide the key technical capabilities and industry resources needed, preventing excessive competition at the PaaS-layer, streamlining the vertical ecosystem, accelerating breakthroughs in applications and solutions, and achieving leadership in both business and scale. This will shape a positive cycle of technology iteration driven by applications and businesses.

The accelerated integration of AI into industry triggered by ChatGPT has made it clear that we must aggregate limited industry resources through top-level design and strategic planning. This will be the only way to continue forward with the asymmetric competition strategy that has defined the mobile Internet era. We should start with smaller models and specialized AI, and collaborate with verticals to achieve joint innovation and breakthrough. Iterative growth and mature AI software, hardware, and foundation model technologies will be achieved through the application and business success of smaller models.

These efforts will finally enable effective growth in new market segments and allow countries, industries, and enterprises to build their competitiveness in the new phase of vertical industry integration, innovation, and transformation.