With the right approach, carriers can use FTTR to enable product and service differentiation, overcome competition from OTT players, and boost their brand equity.

Zhang Jun, Huawei Carrier BG Network Chief Consultant, the Ex-CTO of Shanghai Telecom

China's carriers have deployed or upgraded all access networks with optical fiber over the past decade, representing the first optical-network revolution and laying the foundation for second optical revolution of FTTR.

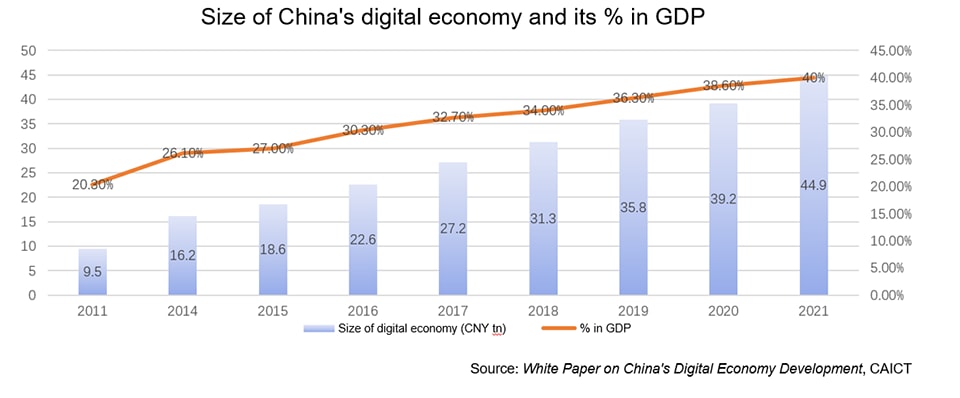

By the end of 2021, China's digital economy had experienced fivefold growth over the preceding decade to reach 44.9 trillion Chinese yuan, transforming the nation into a cyber powerhouse. During that time, the proportion of the digital economy in relation to the national economy doubled from 20% to 40%.

Ⅰ. Strategic value of fiberization

China's “Cyber Powerhouse” strategy began with fiber broadband. In the industrial policy environment of triple play network convergence, Shanghai Telecom took the lead in proposing the "Metropolitan Optical Network (MONET)" strategy in June 2009, prioritizing FTTH network deployment. Based on the successful practice of Shanghai Telecom, China Telecom launched its "Broadband China ▪ Optical Network City" strategy in February 2011. In 2013, "Broadband China" was upgraded to a national strategy.

By the end of 2021, China had more than 500 million broadband users, 94% of whom were fiber broadband users. Of those, 92% were subscribed to megabit bandwidth, while 35 million were subscribed to gigabit bandwidth. By the second quarter of 2022, the number of gigabit users had jumped to 56 million.

Without fiber, neither fixed nor mobile networks can flourish. Fiberization ratios are key indexes for measuring network development, including the ratios of fiber to the home, fiber to the enterprise, and fiber to the base station.

China's carriers have deployed or upgraded all their access networks with optical fiber over the past decade. The first optical-network revolution laid the foundation for China to become a cyber powerhouse. And over the next decade, the second revolution of optical networks will realize the fiberization of home networks and enterprise LANs with fiber to the room (FTTR). It will achieve the development goal of end-to-end full-fiber networks, and further strengthen the position of the Cyber Powerhouse strategy.

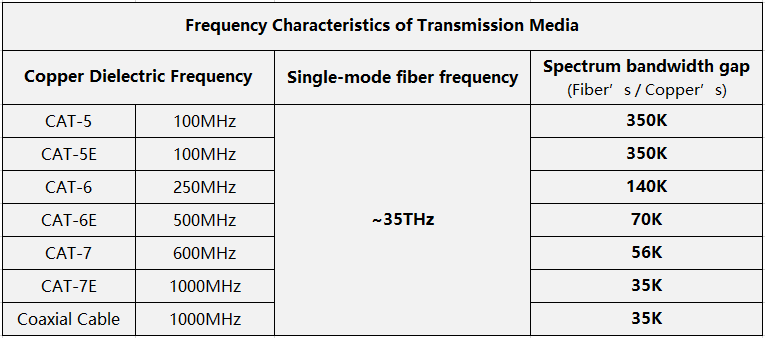

The two basic factors that determine communication bandwidth are the frequency characteristics of the transmission medium, which is the most important parameter, and the corresponding modulation technology. Comparing the frequency characteristics of copper wire and single-mode optical fiber provides many useful insights.

The above table shows that the spectrum capability of fibers can exceed that of copper wire by tens of thousands to hundreds of thousands of times. While the bandwidth potential of copper wires is limited, the potential for fiber is infinite. Due to bandwidth bottlenecks, copper wires need to be upgraded every five to ten years, making network evolution more difficult. In contrast, fiber has a long service life and can be deployed in one go without requiring re-cabling for 30 years. Currently, fiber is the transmission medium that offers the highest bandwidth potential. Compared with copper wires, fiber consumes less energy and is more suitable for achieving green development goals.

Ⅱ. FTTR brings new business value to carriers

From the perspective of carriers, FTTR can bring obvious strategic opportunities in the areas of differentiation, premium quality, and visualization, giving carriers an entry point to home and enterprise LANs. Notably, FTTR is more valuable for SMEs. .

1. Differentiation and Premium Quality

Differentiation is a powerful tool for enterprises to improve competitiveness and achieve sustainable development.

Differentiation in terms of products can maximize value and provide benefits from market segmentation. Differentiation through competition can include different quality offerings at the same price or different prices at the same quality.

In the government and enterprise markets over the past two decades, Chinese carriers have recognized the competitive advantages brought by differentiation in terms of tariffs, quality, bandwidth, protection and recovery, latency, visualization, product differentiation of other value-added services, and differentiation in pre-sale, in-sale, and post-sale capabilities and levels. However, in the home broadband market, much space still exists for differentiation. Current home broadband packages focus on differentiated tariffs and bandwidths, but do not take advantage of quality differences. With the homogeneous competition of home broadband, quality and service differentiation will become more important for home broadband. As one executive of a Chinese carrier noted, there are nearly 300,000 high-income individuals in the city where he lives. They are the potential customers of Home FTTR and can help enhance the brand equity of the carrier.

Brand equity is one of an enterprise’s most important assets and is in turn intrinsically linked to the perception of premium quality. As the FTTH user market of Chinese carriers is approaching saturation, home Wi-Fi networking has become a mainstream method for carriers to enhance customer loyalty and improve competitiveness. Compared with traditional Ethernet cable Wi-Fi, FTTR-based optical cable Wi-Fi delivers superior home-network quality. People perceive optical fiber as representing premium quality, which is the ultimate goal of home networks.

For tier one fixed carriers, FTTR can build up brand equity for their broadband offerings. For tier two and tier three fixed carriers, FTTR can be used as an effective means to overtake competitors. The window of opportunity is determined by differentiated competitive ability. Whoever deploys FTTR first will attract users first, especially high-end users. Opportunity knocks but once.

The carrier I worked at for 30 years launched the "Metropolitan Optical Net" project in 2009 and the "World's First Gigabit City" project in 2016. Were these projects all driven by service demand? Not entirely. At the time, they were oriented not only to service demand, but also to competition. This carrier took the lead in deploying its optical network in order to seize the opportunity of service development, consolidate infrastructure network capabilities, raise the competition threshold, and build up its broadband brand equity. Some people were against the projects at the time, because they were not underpinned by business requirements. But, now they applaud the wise strategic decision. Pipes are always the foundation of carriers, whether fixed or mobile. Numerous successes and failures in history have proven that in the Internet era, bandwidth and latency always represent core competitiveness.

Demand can be stimulated and created. It can be driven by business, competition, technology, investment, or policies. And more recently, even the pandemic has proven to be a driver. Are Chinese 5G and Gigabit optical networks driven by business requirements? In my opinion, they are the sum of the above-mentioned driving forces.

2. Visualization

Compared with traditional Ethernet cable Wi-Fi, FTTR requires communication protocols between the master gateway and slave gateways, which brings visualization to carriers and end-users.

Visualization for carriers: Through NCE-FAN carriers can obtain various fault data from home networks. Through big data analysis, they can remotely guide end users to resolve a large number of faults, reducing O&M costs caused by unnecessary onsite visits. Based on AI analysis of Internet surfing characteristics, carriers can market AI-based application acceleration packages to specified user groups and benefit from providing value-added services (distance education and cloud games, and so on).

Visualization for end users gives controllability of certain functions: Users can use an app to view connection topology, connected terminals, connection types, and connection status on their home network; verify the installation and maintenance quality of carriers; and control the online time and content of various terminals, including games, videos, office work, social networking, and payments. In addition, they can detect the network, device, interference, coverage, configuration, and load status, greatly improving the service experience for end users.

Making, not saving, money is the goal. To make money, expenditure is required. So, reducing procurement costs should not be at the expense of network and service performance and functions, nor should we focus only on procurement costs and ignore O&M costs. Procurement costs are one-off, while O&M costs are long-term and need to be considered systematically.

3. Consolidate the home DICT foundation

On home networks, carriers have advantages in gateway connections and door-to-door services. Carriers compete with OTTs for the entrance of home network connections, while carriers compete with each other in installation and maintenance capabilities, which require better O&M teams and systems.

The home network connection entrance is a core advantage possessed by carriers. However, traditional home Wi-Fi networking solutions, such as ethernet cables, PLCs, and Wi-Fi relays, are used. OTT devices have their own smart home solution ecosystem based on home routers. Therefore, carriers' home network connection entrances are often bypassed by OTT devices, so the advantages of the home gateway cannot be fully utilized. FTTR can completely change this situation. Because communications-specific technology is used between the master and slave FTTR gateways, OTT home routers are not an option. This enables carriers to control access to home network connections through the master gateway of FTTR, consolidating the foundation of home DICT.

Network connectivity is a key advantage of carriers, including Wi-Fi networking, which ensures user experience and door-to-door service awareness. OTT is good at service applications, for example, using a smart speaker at the entrance to implement service control with human-machine interaction. Professionals handling professional issues creates a reasonable and sustainable ecosystem.

4. ToB is more valuable

Historically, one carrier provided a large number of enterprise gateways for small and micro enterprise customers. The purchase price of an enterprise gateway is at least five times higher than the price of a home gateway, but most of these were used in bridged mode. The carrier spent large sums on enterprise gateways, but they did not get any more business opportunities through bridged mode. The reason is that carriers do not provide perfect Wi-Fi networking solutions for enterprises, with the market in fact occupied by third-party ICT integrators.

ToB is more valuable. The FTTR-SME can make full use of the resource advantages of carriers’installation and maintenance services. Through a package solution including cabling, the FTTR-SME can help carriers extend from WAN to LAN and solve the problems of wired and wireless broadband access and providing internal network connections for enterprise customers. Expanding sales scope from a leased line of Internet to enterprise Wi-Fi networking of Intranet services can expand the market space, improve user experience, and enhance customer loyalty. Moreover, carriers' cloud-network synergy resource advantages can be leveraged to meet the cloud migration requirements of enterprise digital transformation, bringing new opportunities for DICT service development.

The home network and SME network are not simple connections of various terminals. They are also a network that needs to be visible, manageable, and maintainable. The FTTR package solution covers not only the gateway itself, but the entire SME and home LAN. Compared with traditional AC+AP and Mesh Wi-Fi networking, FTTR has unmatched advantages in anti-interference capability, roaming handover delay, bandwidth capability, user experience, visibility, manageability, and O&M.

FTTR in China is developing on a large scale. By the first half of 2022, the three major carriers in China had attracted 400,000 FTTR subscribers, a five-fold increase over the second half of 2021. By the end of 2022, this is expected to exceed 2 million. As well as China, more than 20 carriers in West Europe, Asia Pacific, Latin America, and Middle East are very optimistic about the FTTR development direction and are actively conducting pilots, with some specifying their FTTR strategic development goals.

Learn more about Huawei’s FTTR solution.